Overview

This cookbook provides a step-by-step guide to running the PACTA for

Supervisors analysis using the pacta.multi.loanbook

package. The analysis is designed to help financial supervisors assess

the alignment of banks’ loan books with the Paris Agreement goals.

What is the PACTA for Supervisors analysis?

PACTA for Supervisors is based on the PACTA methodology, which assesses the alignment of financial portfolios with climate goals utilizing forward-looking asset-based company data (ABCD) that is linked to financial assets and compares the production profiles of those companies with technology and emissions pathways from climate transition scenarios at the sector and/or technology level.

Who is this tool built for?

The PACTA for Supervisors analysis is primarily designed to be run by financial supervisors on their own, with minimal additional guidance. However, it can also be a useful tool for any other user, in case they would like to run a PACTA analysis on multiple loan books.

The main difference between this tool and the individual PACTA for Banks software packages is that this tool aims to facilitate the analysis of multiple loan books at once, streamlining the process as much as possible, to keep the burden for the user to a minimum. As such it is a helpful tool for anyone who would like to run a PACTA analysis on multiple loan books.

What can the results of the PACTA for Supervisors analysis be used for?

Financial supervisors or regulators can use the results of the analysis to assess the alignment of banks’ loan books with the Paris Agreement goals, to identify sectors where banks may need to take action to improve alignment, and to screen the financial system for potential climate-related transition risks. The analysis can be parameterised in different ways to explore patterns across the analysed loan books. If run by private institutions, the results may additionally be used to identify opportunities for climate-aligned investments, as well as for detecting individual counterparties that may be exposed to climate-related transition risks and may therefore require dedicated focus in the risk management process.

Users will be able to obtain both tabular outputs and plots that can be used for any of the above use cases. The tabular output further enables processing of the alignment results in other models or tools, for example as an input into financial risk models, or as a recurring input into internal monitoring systems.

The level of granularity of the outputs allows for a systematic analysis of climate alignment starting at the financial system level (across all analyzed loan books together), down to the individual counterparty level, and across sectors and technologies. Grouping of the results at any of these levels by additional dimensions can easily be achieved using the configuration file.

What are the main steps of the analysis?

The main steps of the analysis are as follows:

- Data preparation: Prepare the ABCD data and optionally a custom sector split.

- Matching process: Match the raw loan books to the ABCD data.

- Prioritization of loan books; Match success and coverage diagnostics: Prioritize the matched loan books and analyze their coverage.

- Run PACTA for Supervisors analysis: Run the analysis based on the

parameters set in the

config.ymlfile.

This cookbook will guide you through each of the steps of the analysis in detail, explain the required input data sets and software, and provide guidance on how to interpret the results.

Preparatory Steps

This section provides an overview of the preparatory steps that need to be taken before running the PACTA for Supervisors analysis. It includes information on the required input data sets, the required software, and the how to setup the project folder and file structure. Finally, it provides a checklist of the steps that need to be taken before running the analysis, summarizing in brief the steps explained in more detail before.

Required Input Data Sets

The PACTA for Supervisors analysis requires a number of input data

sets to run. Some of these can be obtained from external sources, while

others need to be prepared by the user. Furthermore, some of the input

data sets are optional and there inclusion will depend on the settings

provided in the config.yml file.

The main input data sets required for the analysis are the following:

Asset-based Company Data (ABCD)

- required input

- external source

- XLSX file

This data set provides information on the production profiles and emission intensities of companies active in the following real economy sectors: Automotive (light-duty vehicles) manufacturing, aviation, cement production, coal mining, upstream oil & gas extraction, power generation, and steel production. The ABCD is typically obtained from third party data providers. However, it is possible to prepare the ABCD yourself or complement an external data set with entries that may not be covered out of the box.

The ABCD data set must be an XLSX file and contains the following columns:

company_idname_companyleiis_ultimate_ownersectortechnologyplant_locationyearproductionproduction_unitemission_factoremission_factor_unit

Further information on how to obtain ABCD for PACTA and documentation of the individual sectors and data points can be found here LINK.

Scenario Data

- required input(s)

- external source

- CSV file(s)

The scenario data set provides information on the trajectories of technologies/fuel types and of emission intensities pathways for each of (or a subset of) the sectors covered in PACTA.

For sectors with technology level trajectories, the data set provides the TMSR and SMSP pathways based on the Market Share Approach, an allocation rule that implies all companies active in a sector have to adjust their production in a way that keeps market shares constant and solves for the aggregate climate transition scenario (LINK to the market share documentation).

The target market share scenario data set must be a CSV file and contains the following columns:

scenario_sourceregionscenariosectortechnologyyearsmsptmsr

For sectors that do not have technology level pathways, PACTA uses the Sectoral Decarbonization Approach (SDA), an allocation rule that implies that all companies in a sector have to converge their physical emission intensity at a future scenario value - e.g. in the year 2050. This implies that more polluting companies have to reduce their physical emissions intensity more drastically than companies using cleaner technology. It does not have any direct implications on the amount of units produced by any company (LINK to the SDA documentation).

The SDA scenario data set must be a CSV file and contains the following columns:

scenario_sourceregionscenariosectoryearemission_factoremission_factor_unit

While the raw input values of the scenarios are based on external third party organisations - such as the International Energy Agency (IEA), the Joint Research Center of the European Commission (JRC), or the Institute for Sustainable Futures (ISF) - the input data set for PACTA must be prepared using additional steps, which are documented publicly on the following GitHub repositories:

Since RMI has taken over stewardship of PACTA the prepared scenario files can also be accessed as CSV downloads the PACTA website under the “Methodology and Documents” tab of the “PACTA for Banks” section. The files are usually updated annually based on the latest scenario publications.

Raw Loan Books

- required input

- self-prepared

- CSV file(s)

The raw loan books are the financial data sets that you would like to analyze. They contain information on the loans that banks have provided to companies. As a supervisor, the data required to construct these data sets will typically be available to you through regulatory filings that are accessed via internal data bases or similar. As a bank, the data required will be available in your internal systems.

The raw loan books must be prepared as CSV files and contain at a minimum the following columns:

id_loanid_direct_loantakername_direct_loantakerid_ultimate_parentname_ultimate_parentloan_size_outstandingloan_size_outstanding_currencyloan_size_credit_limitloan_size_credit_limit_currencysector_classification_systemsector_classification_direct_loantakerlei_direct_loantakerisin_direct_loantaker

NOTE: The tool will automatically add a column

group_id to each of the loan books, which uses the file

name as a value. This allows you to group the results the analysis by

loan book, using the by_group parameter in the

config.yml file. For any other variable that you may want

to group the results by, you need to add a column to the raw loan book

files that you then provide as the by_group parameter in

the config.yml file.

For detailed descriptions of how to prepare raw loan books, see the PACTA for Banks documentation and navigate to the “Training Materials” tab of the “PACTA for Banks” section. The “User Guide 2”, the “Data Dictionary”, and the “Loan Book Template” files can all be helpful in preparing your data.

TODO: check if the relevant documents are up to date

Misclassified Loans

- optional input

- self-prepared

- CSV file

The user can provide a list of loans that have been misclassified in the raw loan books. The aim here is specifically to remove false positives, that is, loans that are classified in scope of one of the PACTA sectors, but where manual research shows that the companies do not actually operate within the PACTA scope. Such a false positive may be due to erroneous data entry in the raw loan book, for example. Removing these loans from the falsely indicated sector in the calculation of the match success rate will give a more accurate picture of what match success rate can really be reached.

Asset-Based Company Data (ABCD) for company sector split

- optional input

- external source

- XLSX file

In case the user wants to split company exposures across sectors of in scope activity, the user must provide a version of the ABCD data set that follows the format of the Advanced Company Indicators data set by Asset Impact. This data set includes power generation values which are required for the primary energy based sector split.

Companies to apply primary energy split on

- optional input

- self-prepared

- CSV file

When applying the sector split on company exposures, the user can provide a list of companies for which the sector split should be based on primary energy content. For all other companies, a simple equal weights split will be applied. For more information on the sector split, see the documentation.

TODO: Move the sector split documentation to this repo!

Required Software

Using the pacta.multi.loanbook package for the PACTA for

Supervisors analysis requires the following software to be installed on

your system:

R (version 4.1.0 or higher)

R is the programming language that the

pacta.multi.loanbook package is written in. You can

download R from the Comprehensive

R Archive Network (CRAN).

RStudio (optional)

RStudio is an integrated development environment (IDE) for R

developed by Posit. It is not strictly required to run the analysis, but

it can be helpful for managing your project and running the analysis.

Generally, RStudio is very widely used among the R cummunity and

probably the easiest way to interact with most R tools, such as

pacta.multi.loanbook. RStudio Desktop is an open source

tool and free of charge. You can download RStudio from the Posit RStudio website.

pacta.multi.loanbook R package

The pacta.multi.loanbook package is the main software

tool that you will use to run the PACTA for Supervisors analysis. You

can install the package from the RStudio

CRAN mirror by running the following command in R:

install.packages("pacta.multi.loanbook")Alternatively, you can install the development version of the package from GitHub by running the following command in R:

pak::pak("RMI-PACTA/pacta.multi.loanbook")Required R packages

The pacta.multi.loanbook package depends on a number of

other R packages. These dependencies will be installed automatically

when you install the pacta.multi.loanbook package. The

required packages are:

cli (>= 3.2.0), config, dplyr, ggplot2, glue, networkD3, r2dii.analysis (>= 0.3.0), r2dii.data (>= 0.5.0), r2dii.match (>= 0.2.0), r2dii.plot (>= 0.4.0), readr (>= 2.0.0), readxl, rlang, scales, tidyr, webshot, withr, yaml, yesno

Suggested R packages

The suggested packages are not required to run the analysis, but they are used in the examples and vignettes provided with the package:

gt, knitr, pkgdown, rmarkdown, usethis, testthat (>= 3.1.9), tibble, writexl

FAQ

How do I install the pacta.multi.loanbook package?

The most common ways to install R packages are via CRAN or GitHub. Public institutions often have restrictions on the installation of packages from GitHub, so you may need to install the package from CRAN. In some cases, your institution may mirror CRAN in their internal application registry, so you may need to install the package from there. Should you have any issues with the installation from the internal application registry, it is best to reach out to your IT department. If you cannot obtain the package any of these ways, please reach out to the package maintainers directly for exploring other options.

How do I install the required R packages?

In principle, all dependencies required to run the

pacta.multi.loanbook package will be installed

automatically when you install the package. However, if you encounter

any issues with the installation of the required packages, you can

install them manually by running the following command in R, where …

should be replaced with the package names from the list above, separated

by commas:

install.packages(c(...))Project Setup

Config

All of the functions needed to run a PACTA for Supervisors analysis

take a config argument, which can either be a path to a

config.yml file (see vignette("config_yml"))

or a config list object containing previously imported settings from a

config.yml file. All of the settings/options are configured

with this config.yml file.

Input/Output folder structure

The config.yml file then points to an input directory

and to four output directories, one for each user-facing function, that

the user can choose anywhere on their system, as long as R has read and

write access to these directories. A recommendable choice to structure

an analysis project would be to place all these folders and the

config.yml file in a project folder. The input folder must

contain all input files as described above, with the raw loan books

being placed in a sub-directory that must be named

"loanbooks". The output folders will automatically be

created at the locations indicated in the config.yml file.

They will be populated by running the analysis. NOTE:

Re-running a step of the analysis will replace the entire corresponding

output directory, if the directory already exists.

An example of how the project folder could be structured:

project_folder

├── config.yml

├── input

│ ├── ABCD.xlsx

│ ├── loanbooks

│ │ ├── raw_loanbook_1.csv

│ │ ├── raw_loanbook_2.csv

│ │ └── ...

│ ├── scenario_data_tms.csv

│ ├── scenario_data_sda.csv

│ └── ...

├── prepared_abcd

├── matched_loanbooks

├── prioritized_loanbooks_and_diagnostics

└── analysisNotice that the names of the directories can be changed to something the user may prefer. The names were chosen for illustrative purposes to reflect the corresponding user-facing functions that create the outputs.

Running the Analysis

This section provides a step-by-step guide to running the PACTA for

Supervisors analysis using the pacta.multi.loanbook

package. It includes information on the structure of the workflow, the

required functions, and the interpretation of the results.

Structure of the Workflow

The PACTA for Supervisors analysis consists of four main steps:

- Data preparation: Preparing the input data sets for the requirements of the analysis.

- Matching process: Matching the raw loan books to the ABCD data and validating the matches manually.

- Prioritization of loan books: Selecting the correct matches for further analysis and diagnosing match success and coverage statistics

- Run PACTA for Supervisors analysis: Running the analysis based on

the parameters set in the

config.ymlfile to generate the production-based alignment analysis.

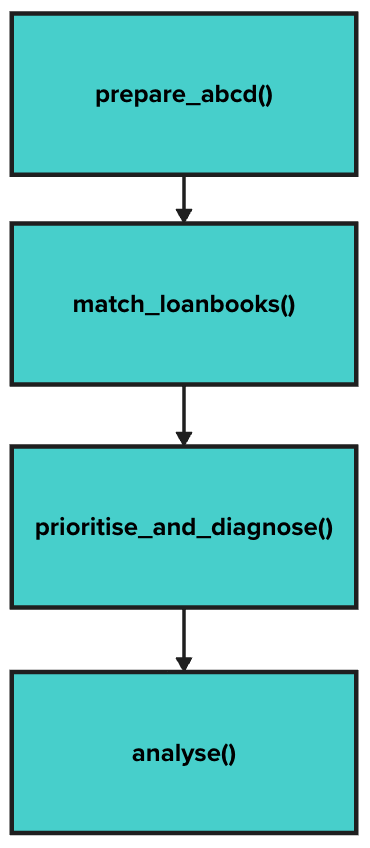

The following diagram illustrates the structure of the workflow:

Fig. 1: Structure of the Workflow

As the diagram shows, there is a logical sequence to how to run the

functions. For any of the functions to work, the previous functions must

have been run already and their outputs must be accessible as inputs to

the next functions. If you want to keep different versions of the

calculations, i.e. you want to avoid overwriting past outputs, you will

have to (1) ensure that each run is done with a new value for the

corresponding output directory set in the config.yml and

(2) that the relevant function refers to the appropriate directories of

upstream outputs. For example, if you want to run the analysis twice and

keep both results, all dir_* entries of the

config.yml should remain identical for both runs, except

for the dir_analysis entry, which should be different for

each run.

The following sub sections will provide detailed information on each

of the steps of the analysis, starting with a brief explanation of the

setup, as each of the functions will require the path to the

config.yml file as an input argument.

Setup

If you run PACTA for Supervisors interactively or from a script you

may have prepared, you will likely want to load the

pacta.multi.loanbook package and save the path to the

config.yml file in a variable first:

library(pacta.multi.loanbook)

config_path <- "config.yml"This allows you passing the relevant config information easily to each of the four main functions.

Data preparation

The first step of the analysis is to prepare your input data sets for

the requirements of the analysis. Your ABCD data will need to be

prepared and you can optionally use a custom sector split, that will

also need to be prepared. The relevant function is

prepare_abcd(), which takes configurations from the

config.yml that you have prepared. The function will store

intermediary files in the directory that you have indicated as the value

corresponding to the key dir_prepared_abcd in the

config.yml. This step only has to be run once for an

analysis. You can run this function as follows:

pacta.multi.loanbook::prepare_abcd(config_path)Options for the prepare_abcd() function

The prepare_abcd() function has a number of options that

can be set in the config.yml file. These options

include:

- whether or not inactive companies should be removed from the ABCD

data (For more information on the options available, see the relevant

section on preparing the ABCD in the

vignette("config_yml").) - if and how a company sector split should be applied in the

calculations (For more information on the options available, see the relevant

section on the sector split in the

vignette("config_yml")). Additionally, see the documentation of the sector split methodology.

Matching process

The next step in the analysis is to run the matching process.

Assuming you have prepared the raw loan books as explained in the section on preparing the input

data sets, you can now use the match_loanbooks()

function. This will read the raw loan books from your inputs and attempt

to match them to the prepared ABCD data from the previous step. The

function will store matched loan book files in a directory that you have

indicated as the value corresponding to the key

dir_matched_loanbooks in the config.yml. You

can run this function as follows:

pacta.multi.loanbook::match_loanbooks(config_path)After the matching process is complete, you will need to do some manual matching. This means that you will need to manually inspect the suggested matches that the tool has found and decide which ones to keep or to remove. This is especially important when using text based matching, as there is no guarantee that similar company names as identified by the algorithms will actually refer to the same companies in the raw loan books and the ABCD. Thus, a manually validation step is crucial in the analysis, as the quality of the matches will determine the quality of the results of any further calculations.

The manual matching process is not automated and will require some

time and effort on your part. You can find the matched loan books in the

.../matched_loanbooks folder. The matched loan books will

be stored in CSV files, one for each raw loan book. You can open these

files in a spreadsheet program to verify the matches. Importantly, you

will need to make a copy for each of the matched loan book files in the

same .../matched_loanbooks folder and rename that copy by

adding the suffix _manual to the file name. The following

steps of the analysis expect this pattern, so it is important to follow

this naming convention.

You can find more detaied information about the matching process in the training material on the PACTA for Banks website in the section “PACTA for Banks Training Webinar 2” and in the corresponding slide deck.

Some expectations for the matching process

- It is unlikely that you will be able to match all of the loans from

your raw loan books to the ABCD data set. This is expected and has the

following reasons:

- Raw loan books often include companies that are not in scope of the PACTA analysis, for example there may be companies active in the financial sector or in manufacturing of IT products. Both these sectors are fully out of scope. There may also be companies that are active in upstream or downstream activities of the sectors covered by PACTA. This means that the company activities are not at the part of the value chain that is covered my PACTA and accordingly the companies are not matched. Examples for this are power distribution companies or companies that manufacture air crafts.

- The ABCD data set may not cover all companies that are in scope of the PACTA analysis. While coverage of the real economy sectors is usually rather high in the data sets that are commonly used for PACTA, there are gaps. This implies that some in-scope companies cannot be matched because the ABCD data set does not include them. Advanced users may research the production profiles of such companies by themselves and add them to the ABCD data manually, however this is a very involved process and not standard procedure and will therefore not be covered in this cookbook.

- If you are using sector classifications for the matching process (which is recommended whenever possible), some matches may not be identified in case the companies in the raw loan book are misclassified. For example, if a utility that is focused on coal-fired power generation is classified as a coal mining company, the matching function will not suggest a match.

- Given that it is unlikely to match all loans, it is recommended to try and match the companies with the largest financial exposures first, as this ensures the best possible financial coverage of the loan book in the analysis.

- It is also recommended to run multiple iterations of the matching

process, potentially adjusting the matching parameters in the

config.ymlfile, to see if you can improve the match success rate. The match success rate can be obtained based on the manually validated matched loan books and the raw loan books as described in the next section on prioritization and diagnostics.

Options for the match_loanbooks() function

The match_loanbooks() function has a number of options

that can be set in the config.yml file. These options

include:

- specifications for the approach to matching the raw loan book with

the ABCD relevant

section on matching in the

vignette("config_yml")). Note that these parameters are all based on ther2dii.match::match_namefunction and pass the parameters directly to that function. For more information on the options available, see the documentation of the r2dii.match package. This also covers matching based on unique identifiers, which is the most reliable way to match companies, but requires that both the raw loan books and the ABCD contain such identifiers. - whether to use a manually prepared sector classification system for

matching the loan books to in-scope PACTA sectors, see the relevant

section on matching in the

vignette("config_yml")), or not. If not, the sector classification systems provided inr2dii.data::sector_classificationscan be used.

Addressing misclassfied loans

There are two ways to appropriately handle misclassified loans that are identified as in-scope in the raw data set but are then not matched.

- Correct the classification in the raw loan book and re-run the matching process. If the loan was clearly mis-classified, this may be the most appropriate way to handle the issue. It may be a good idea to record any such changes made in the input data though. The upsdie of this approach is that the loan will now either be matched correctly, as it will be assigned the sector that the company should have and therefore find an entry in the ABCD data set to match against. Or, if there is still no match to be found in the ABCD, the loan will correctly be missing in the appropriate sector and therefore indicate a lower match success rate where it should.

- If a manual re-classification of the raw loan book is not possible

or desired, the calculation of the match success rate can be corrected

by adding a file

loans_to_remove.csvto the input directory. This file should include the columnsid_loanandgroup_idto indicate the precise mis-classified loan and the loan book in which it was found. This combnation of loan and loan book will then be excluded from the match success calculation.

The reason why it is a good idea to either correct mis-classified loans or disregard them in the calculation of the match success rate is that a mis-classified loan cannot possibly be matched in a given sector. Therefore, no amount of work would be sufficient to improve the sector match success rate, because it is calculated against an incorrect baseline. Technically, the user is not forced to correct misclassifications, and there may be a limit to how much time should be spent on this, but it is recommended to at least correct large mis-classified loans.

Prioritization of loan books; Match success and coverage diagnostics

The next step is to prioritize the manually verified matched loan books and analyze their coverage, both relative to the raw loan book inputs (the “match success rate”) and to the production capacity in the wider economy (the “loan book production coverage”). Prioritizing the loan books means that you will only keep the best identified match for each loan and use that in the following steps of the analysis.

You will probably want to check the status of your loan book and

production coverage several times, as it is rare to get to the desired

level of matching in one iteration. This means you may want to repeat

the previous step (matching the loan books, likely using different

parameters for different iterations) and this step (prioritizing the

matched loan books and analyzing their match success rate) a number of

times to reach the best possible outcome. To prioritize your matched

loan books and calculate display the coverage diagnostics, you will use

the prioritise_and_diagnose() function. This call will

store matched prioritized loan book files and coverage diagnostics in a

directory that you have indicated as the value corresponding to the key

dir_prioritized_loanbooks_and_diagnostics in the

config.yml. You can then run the function as follows:

pacta.multi.loanbook::prioritise_and_diagnose(config_path)Options for the prioritise_and_diagnose() function

The prioritise_and_diagnose() function has a number of

options that can be set in the config.yml file. These

options include:

- the option to set a specific order for prioritizing the matches.

This is an option that is passed directly to the

r2dii.match::prioritizefunction.NULLis a valid default value and is usually a setting that works well, at least as a starting point. For more information, see the relevant section on the prioritization of matched loan books in thevignette("config_yml")or the documentation of the r2dii.match::prioritize() function here.

Run PACTA for Supervisors analysis

The final step is running the analysis based on the parameters you

have set in the config.yml file. This entails both a

standard PACTA for Banks analysis and the calculation of the net

aggregate alignment metric. For both parts of the analysis, outputs will

be stored in the sub-directories ../standard/ (for standard

PACTA for Banks results) and ../aggregated/ for the net

aggregate alignment metric directory - below the directory that you have

indicated as the value corresponding to the key

dir_analysis in the config.yml. Outputs in

these sub directories will comprise tabular outputs and plots. To run

the analysis on all of your previously matched and prioritized loan

books, you will use the analyse() function as follows:

pacta.multi.loanbook::analyse(config_path)Options for the analysis() function and the overall

analysis

The analysis() function has a number of options that can

be set in the config.yml file. These options include:

- which source should be used for allocating climate transition

scenario pathways to the companies and loan books. This refers to the

relevant scenario publication and usually contains the name and the year

of the publication, e.g.:

"weo_2023"or"geco_2023". - which scenario should be used for reference in the net aggregate alignment metric. This must be a scenario that is included in the source indicated above.

- which region to use as a reference for the analysis. This will filter the underlying production capacity to assets in the relevant region and will measure alignment against the scenario trajectory for the relevant region. It must therefore be a region, for which scenario data is available in the source selected above.

- the start year of the analysis. This must be a year that is available both in the ABCD data and for which the scenario data has been prepared. The loan book data is assumed to be a snapshot of the end of the same year.

- the time frame of the analysis, which refers to the number of forward looking years after the start year that are to be considered in the alignment analysis. Usually this time frame is set to 5 years. Specifically, it must be a time frame for which scenario data values and ABCD data values are available for all sectors that are to be analyzed. There are not many cases, in which it is expected to change the time frame to something else than its default value of 5 years.

- by which variables to group the loan books to produce grouped

results of the analysis. This parameter is used across multiple steps of

the analysis, both in the diagnostics and in the analysis. This is

because it slices and/or aggregates the loan books such that the

analysis will produce results along the indicated dimension. If no

by_groupparameter is passed (i.e.NULL), all loan books will be aggregated. Otherwise, loan books can either be kept separate (group_id) or grouped by any other variable that is provided in each of the raw loan books.

All these options are documented in more detail the section

on project parameters in the

vignette("config_yml").

Usually, it will be interesting to run the analysis for more than one by_group, possibly also for multiple combinations of the other parameters. You will therefore have to run the analysis as many times as there are combinations of interest that you wish to generate results for.

Interpretation of Results

Running the analysis will produce a number of outputs that can be used to gain insights into the alignment of financial institutions with climate transition scenarios and to approximate transition risk. The two main pieces of the analysis are the PACTA for Banks analysis and the net aggregate alignment metric. The PACTA for Banks analysis will provide insights into the alignment of the financial institution with the climate transition scenarios for each of the sectors covered by PACTA. The net aggregate alignment metric is intended be used as a high level overview alignment metric for the financial sector. The analyses thus complement each other where the net aggregate alignment metric can serve as a starting point to identify sectors or groups of financial institutions that seem to require particular attention. The PACTA for Banks analysis can then be used to drill down into the details of the alignment of the financial institution with the climate transition scenarios.

The following sections will provide an overview of results that are generated using this analysis and how to interpret them. It will briefly explain each of the relevant metrics, it will mention the plots that correspond to the metrics, and it will explain how the output data sets map to the values shown in the plots. The same will be provided for the coverage statistics that are generated for the analysis.

Coverage Diagnostics

The coverage diagnostics include both a comparison of the number and value of matched loan books with the raw loan books and a comparison of the production capacity of companies in the matched loan books with the production capacity of companies in the wider economy. The coverage diagnostics are intended to provide insights into the quality of the matching process and the coverage of the loan books in the analysis.

Match Success Rate

The match success rate is calculated per sector and can be calculated based on either of the number of loans, the outstanding value of the loans, or the credit limit of the loans. In either case, the sum value of the matched loans is compared with that of the raw loan books.

The output data set contains all three versions of the metric and can

be found in the

../prioritized_loanbooks_and_diagnostics/lbk_match_success_rate<...>.csv

file, where <…> will be replaced with the name of the variable set

in the by_group parameter.

Example Plots Match Success Rate

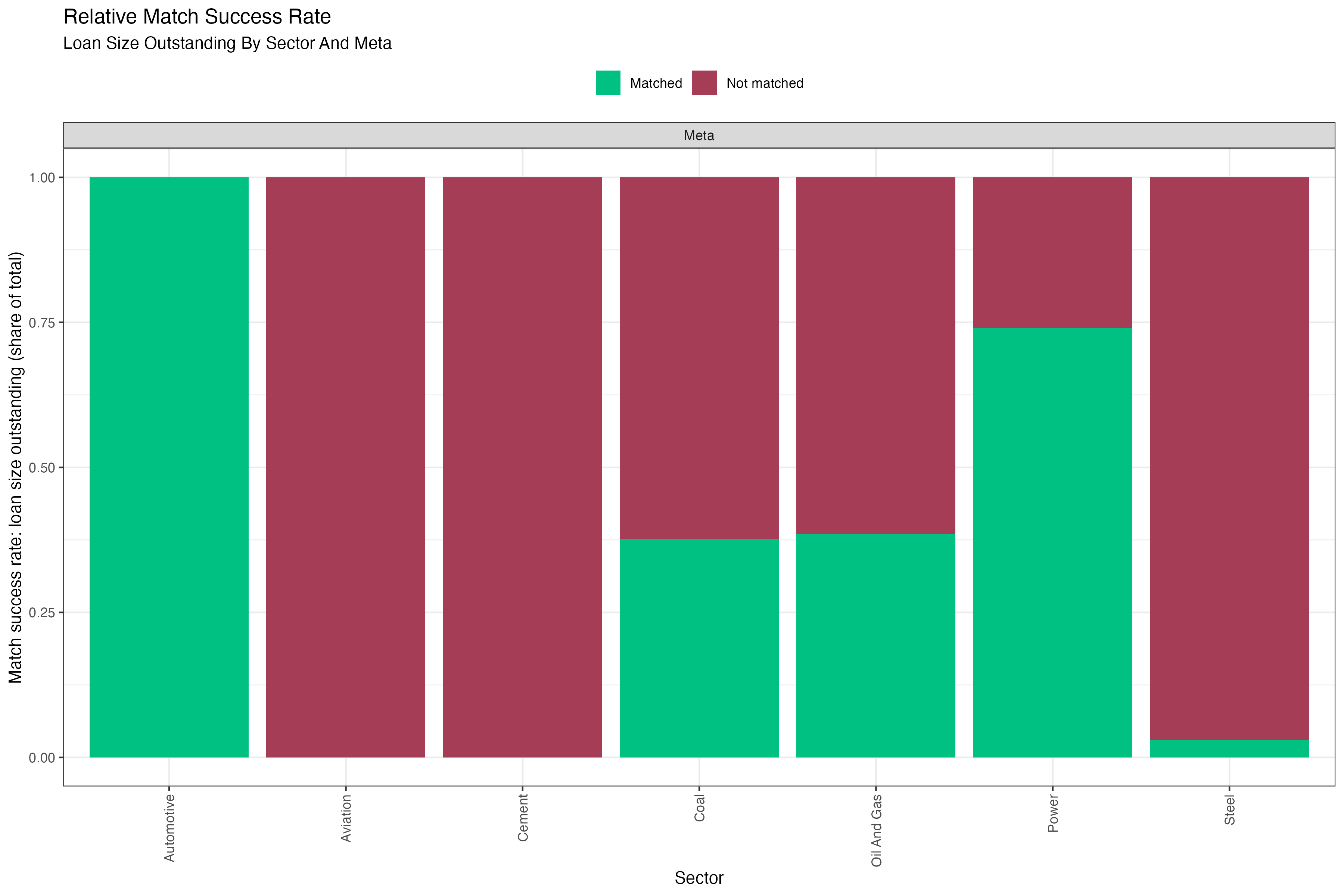

An example plot of the match success rate for the number of loans, in this case grouped by banks types (credit unions, less significant institutions and significant institutions), can look as follows:

Fig. 2: Relative match success rate in number of loans by different bank types. Data is based on simulated test loan books.

Fig. 3: Absolute match success rate in number of loans by different bank types. Data is based on simulated test loan books.

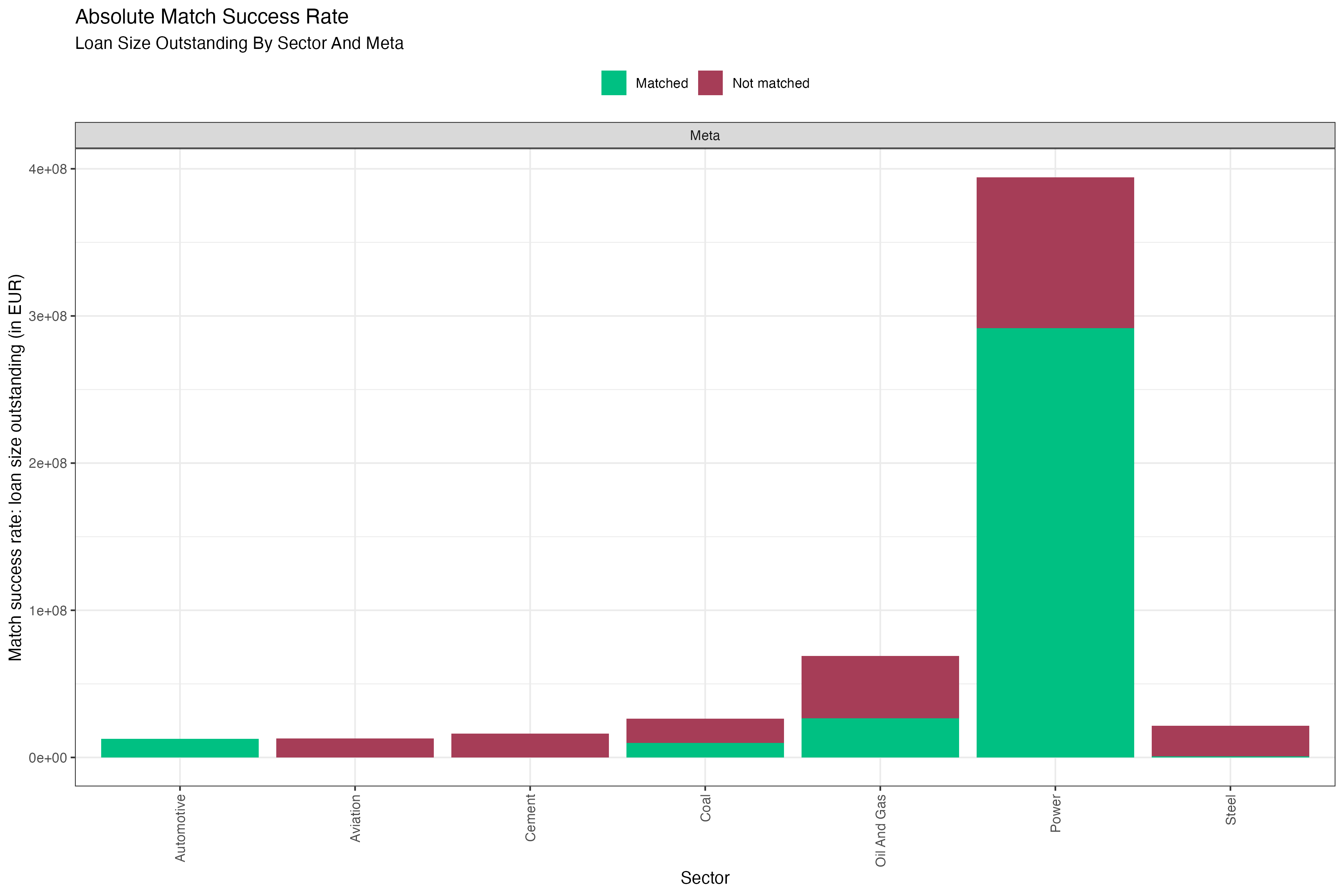

Another example plot of the match success rate for the loan size outstanding, in this case an ungrouped meta view on the entire set of analyzed loan books, might look like this:

Fig. 4: Relative match success rate in number of loans aggregated over all loan books. Data is based on simulated test loan books.

Fig. 5: Absolute match success rate in number of loans aggregated over all loan books. Data is based on simulated test loan books.

Interpretation of the Match Success Rate

The match success rate is a coverage metric of properly identified loans relative to the raw input loan books. It is always provided by sector, because a company in the loan book can only be expected to be matched to the ABCD if it operates in the same sector. Since PACTA only covers a subset of economic sectors, judging the success of the matching process should only take into account the loans that fall within the scope of the PACTA analysis. Of course, the extent of exposure to these sectors may vary significantly between input loan books. But this has more to do with the strategy of the bank than with the quality of the matching process.

Generally, it is desirable to reach as high a match success rate as possible for each sector. It was mentioned before that the time spent to maximize the match success rate is at the discretion of the user. However, it is recommended to aim for a match success rate of more than 80% of the loan value within each sector that you are interested in. The steps to achieve this are described in the section on the matching process LINK.

If after following and concluding the matching procedure the match success rate is high for a given sector or the entire loan book, this indicates that you can draw conclusions from the PACTA analysis for the loan books with higher confidence. If it remains low for some sectors, this can point to one of several issues:

- There may be data quality issues in the raw loan book. For example, the company names may have been entered wrongly, or the sector classification may be incorrect. Problems with the sector classification may be corrected to some degree through desk research. However, there are limits to inferring sector codes like that and it is a time consuming process.

- There may be coverage issues in the ABCD. It is possible that all entries in the raw loan book are correct and the match success rate remains low, because the companies the loan book is exposed to are not covered in the ABCD. Since the ABCD is an externally sourced data set, there are two main approaches to tackling this. One is to reach out to the data provider and try to understand/add the missing data points. The other is to try and add the relevant data points manually based on your own data or research. This is a very involved process and not standard procedure and will therefore not be covered in this cookbook. Beyond those options, it is recommended to highlight coverage issues, if they cannot be fixed.

Data Dictionary Match Success Rate

The underlying data set used to generate these plots contains the following information:

Mapping the Data Dictionary to the Match Success Rate Plots

The variables in the table map to the figures as follows:

-

<by_group>:The variable that the loan books are split by. This determines the number of panes in the plot. E.g. in figures 2 and 3, the loan books are split by bank type, generating one pane per type. In figures 4 and 5, the loan books are not split by any variable, generating a single pane for the entire set of loan books. -

sector: The match success rate is analysed by sector, with the sectors shown in separate columns. This is because a loan in the raw loan book can only be matched to the ABCD if the company operates in the sector covered by the ABCD. This highlights the importance of good data quality in the sector classification of the raw loan book. The target should be to have a sufficiently high match success rate for any sector that you want to make robust statements about. -

match_n: When showing the absolute number of loans matched (figure 3), this determines the size of the matched part of each column. -

total_n: When showing the absolute number of loans matched (figure 3), this determines the total size (matched + unmatched) of each column. -

match_success_rate_rel: When showing the relative number of loans matched (figure 2), this determines the size of the matched part of each column. -

match_outstanding: When showing the absolute matched value of loans outstanding (figure 5), this determines the size of the matched part of each column. -

total_outstanding: When showing the absolute matched value of loans outstanding (figure 5), this determines the total size (matched + unmatched) of each column. -

match_success_outstanding_rel: When showing the relative matched value of loans outstanding (figure 4), this determines the size of the matched part of each column. -

match_credit_limit: When showing the absolute matched credit limit of loans (not shown in figure), this determines the size of the matched part of each column. -

total_credit_limit: When showing the absolute matched credit limit of loans (not shown in figure), this determines the total size (matched + unmatched) of each column. -

match_success_credit_limit_rel: When showing the relative matched credit limit of loans (not shown in figure), this determines the size of the matched part of each column.

Loan Book Production Coverage

The loan book production coverage is calculated per sector and region

(for all regions available in the given scenario_source).

For a given combination of sector and region, it provides the total

number of companies with operations in the sector and region in the

wider economy. It then provides the number of matched companies in the

loan book with operations in that sector and region. A ratio of the two

values tells you the share of companies in the sector and region that

you have identified in the matched loan book. Similarly, the data set

provides the total production capacity of a sector in a region in the

wider economy and the production by companies in the matched loan book

in that sector and region. Notice that it only matters THAT the company

was matched in the loan book, NOT how large the granted loan is. The

ratio of the two values then tells us what percentage of the production

capacity of a sector in a region the financial institution is involved

in. Again, being involved in that production capacity is decidedly not a

full responsibility, because many matched companies will likely have

additional sources of funding. Lastly, the output provides the sum of

the loan size outstanding to the matched companies in each of the

sectors and regions.

The output data set can be found in the

../prioritized_loanbooks_and_diagnostics/summary_statistics_loanbook_coverage<...>.csv

file, where <…> will be replaced with the name of the variable set

in the by_group parameter.

Interpretation of the Loan Book Production Coverage

The loan book production coverage is a coverage metric of the production capacity of companies in the loan book relative to the production capacity of companies in the wider economy. It is always provided by sector and region. Comparisons across sectors need to be separate, because of differing output units. And the coverage by region allows highlighting the regional focus of a bank for the given sector. The production coverage compares matched companies only, hence it depends on the quality of the matching process and any statements about the share of economic activity covered by the matched loan book should take this relationship into account.

Assuming a solid match success rate, the loan book production coverage tells you if the loan book is exposed to a large share of production capacity within a certain sector and region. This information can be relevant when assessing the impact of regional economic trends and policies that may affect the sector. For example, the loan book more susceptible to transition risk in one region than in another even when the introduced policies are very similar, because companies financed may operate a larger share of the production capacity in the first region.

PACTA for Banks Outputs and Graphs

Below you will find a description of the standard PACTA for Banks data outputs and graphs. Some of the data outputs are intermediate files that do not directly map to a plot. These are only mentioned briefly. A detailed description can be found in the data dictionary. The plots are discussed in more detail, including the relevant table from the data dictionary and how the variables map to the plots.

Target Market Share Results

The target market share results provide the intermediate format

output required to generate the technology mix and volume trajectory

plots. The output data set can be found in the

../analysis/standard/tms_results<...>.csv file, where

<…> will be replaced with the name of the variable set in the

by_group parameter.

More information on the target market share results data set can be found in the data dictionary.

Technology Mix

The technology mix metric compares the technology mix of the

production capacity of companies in the loan book with that of the

production capacity of companies in the wider economy and the scenario

technology mix five years into the future. The output data set can be

found in the

../analysis/standard/<...>/data_tech_mix_<sector>.csv

file, where <…> will be replaced with the names of each of the

groups in the variable set in the by_group parameter. This

means that the technology mix results always only show results for one

group at a time.

The technology mix can only be calculated for sectors that have technology level scenario pathways. Generally, those tend to be sectors for which scalable low carbon alternatives exist. The technology mix can also be calculated for sectors in which all technologies are projected to phase down or out, but the results are less meaningful in those cases, as the technology mix cannot show the absolute requirements for a phasedown.

LINK to some more general tech mix explanation?

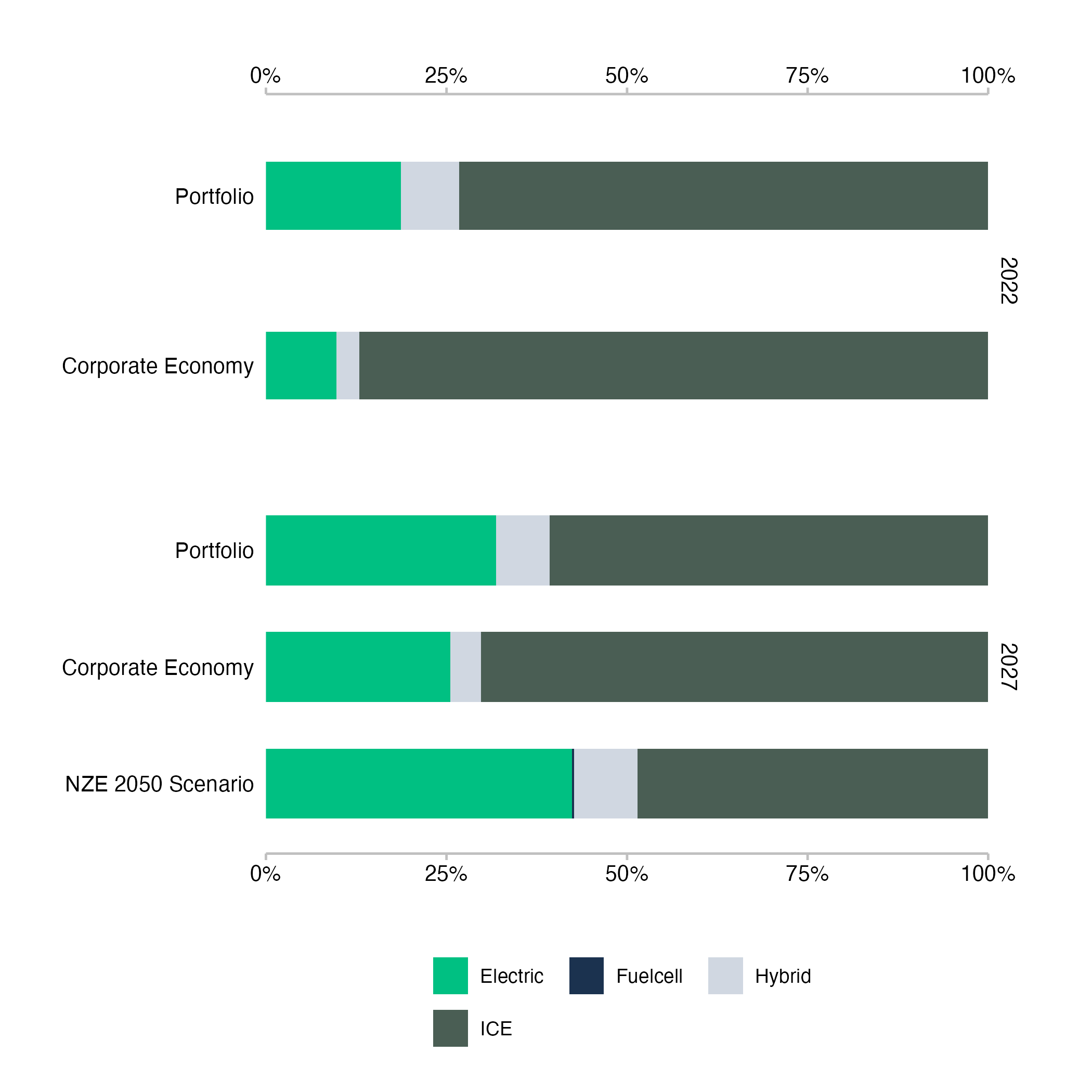

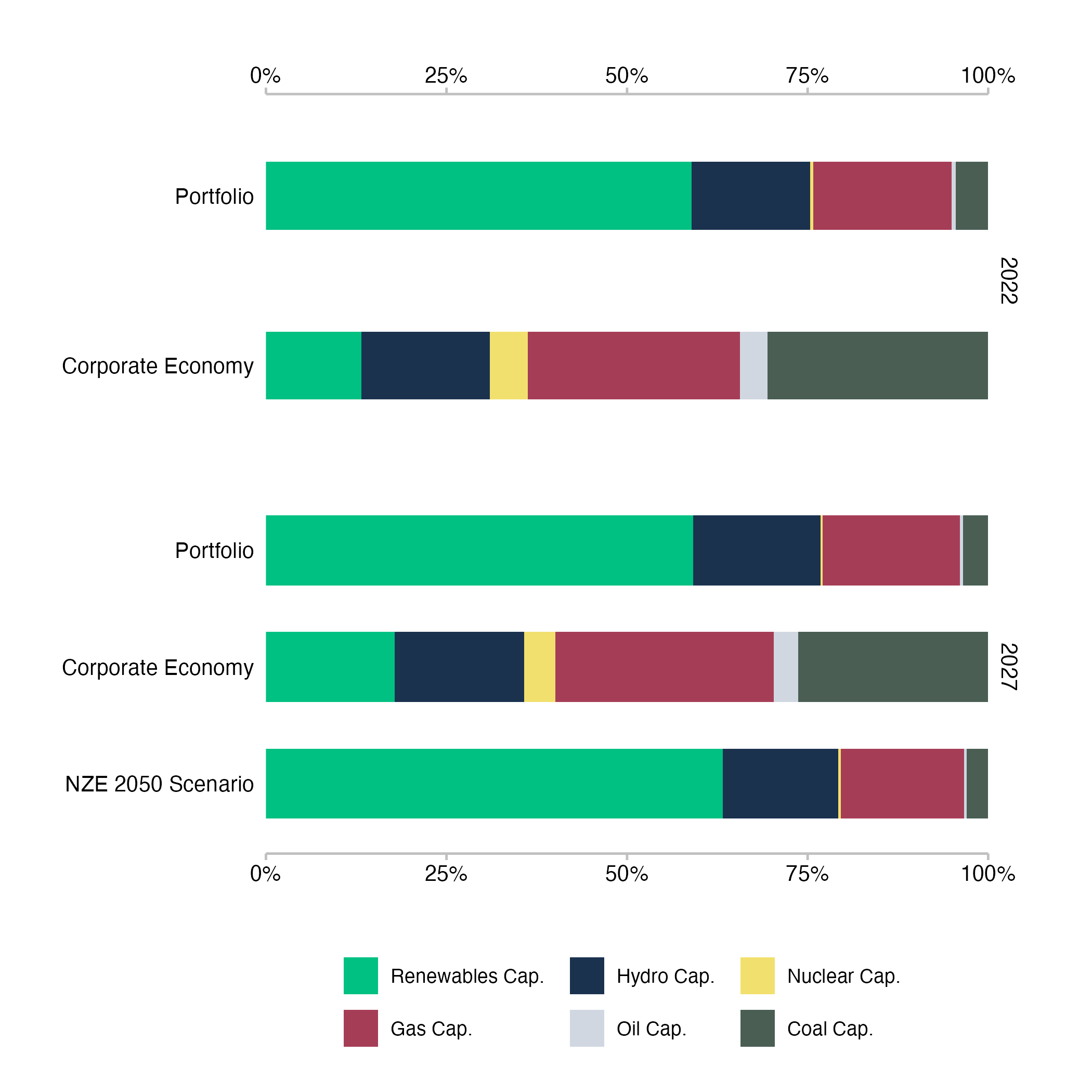

Example Plots Technology Mix

This plot shows the technology mix for the automotive sector of a loan book. We can see that the exposure to automotive production of different engine types in the loan book shifts from 2022 to 2027. The exposure to electric vehicle production increases, while the exposure to internal combustion engine production decreases. A similar shift can be observed in the wider economy, although the shift starts from a smaller share in 2022, which implies the companies that are being financed have a relatively strong focus on electric vehicle production compared to the overall economy. We can also see what the technology mix looks like for the scenario in 2027. In this case, the shift of automotive production from internal combustion engines to electric vehicles in the portfolio exposure is not as strong as it ought to be to be in line with the scenario.

Fig. 6: Technology mix for the automotive sector of a loan book. Data is based on simulated test loan books.

In another example of the technology mix plot for the power sector, we can again see a loan book that is exposed to a much higher share of low carbon technologies than the wider economy, mainly due to the large exposure to companies operating renewable energy power. The plot shows only a marginal shift for the loan book between 2022 and 2027, which means that the share of technologies does not quite align with the scenario values in 2027. However, we can again see that the loan book as far ahead of the wider economy in terms of low carbon technology exposure in the power sector, with nuclear power being the only notable exception of smaller exposure in the loan book.

Fig. 7: Technology mix for the power generation sector of a loan book. Data is based on simulated test loan books.

Interpretation of the Technology Mix Plots

The technology mix plots show the exposure to underlying technologies by sector, where the technology mix of the financed companies is combined using the portfolio weight of each loan to generate the aggregate technology mix at the loan book level. This means that a technology mix at the company level reflects the underlying production of the company in terms of real economic output units, whereas the technology mix at the loan book level reflects the financial exposure of the bank to these technologies through its lending activities. As such, the overall size of the production activities of the underlying companies does not impact the technology mix of the loan book. It is a weighted average of relative production numbers. The technology mix at the loan book level therefore works better as a risk indicator than as a measure of impact.

For the corporate economy bars, the technology mix is based on the unweighted sum of underlying physical production capacity and for the scenario bar, the technology mix is based on the initial technology mix of the portfolio, extrapolated with required changes based on the market share approach that assumes all companies maintain their overall production shares in the sector.

Data Dictionary Technology Mix

The underlying data set used to generate the technology mix plots contains the following information:

Mapping the Data Dictionary to the Technology Mix Plots

The variables in the table map to the figures as follows:

-

<by_group>:The variable that the loan books are split by. This determines the group for which the tech mix is shown. E.g. in case the aggregate loan book is displayed as in figures 6 and 7, the variable and value will be “meta”. If the calculation had been grouped bybank_type, the resulting plots would have been returned for groups, such as credit unions, less significant institutions and significant institutions. -

sector: The PACTA sector that the technology mix is shown for. -

technology/label_tech: The technology represents the differences in product or fuel type (depending on the sector). Generally, some of the technologies within a sector are considered low carbon technologies and others are considered high carbon technologies. The technology mix shows the current distribution across these technologies and how that distribution may change. Thelabel_techis the same as thetechnology, but with a more human readable name to be displayed in the plot. -

year: The technology mix chart uses values from the start year of the analysis and contrasts them with values from the end year of the analysis, usually five years into the future. -

metric/label: The metric differentiates the types of bars shown in the technology mix plot.projectedrefers to the technology mix of the exposures in the loan book,corporate_economyrepresents the production technology mix of the real economy for the selected region andtarget_<scenario>refers to the technology mix the loan book would need to achieve five years into the future in order to be aligned with the scenario based on the market share approach.<scenario>stands for the selected target scenario as set in theconfig.ymlfile. Thelabelis the same as themetric, but with a more human readable name to be displayed in the plot. -

technology_share/value: The actual value that determines the size of each of the technologies in the bars of the plot. Thetechnology_shareis the share of the technology in the total production capacity of the sector in the region. Thevalueis the same as thetechnology_share, but formatted for display in the plot.

Production Volume Trajectory

The production volume trajectory metric compares the future

production capacity in a given technology of the companies in the loan

book with that of the companies in the wider economy and the scenario

trajectories for the loan book five years into the future, based on the

market share approach. The output data set can be found in the

../analysis/standard/<...>/data_trajectory_<sector>_<technology>.csv

file, where <…> will be replaced with the names of each of the

groups in the variable set in the by_group parameter. This

means that the production volume trajectory results always only show

results for one group at a time.

The production volume trajectory metric can only be calculated for sectors that have technology level scenario pathways. Generally, those tend to be sectors for which scalable low carbon alternatives exist, or sectors in which all technologies are projected to phase down or out.

LINK to some more general volume trajectory explanation?

Example Plots Production Volume Trajectory

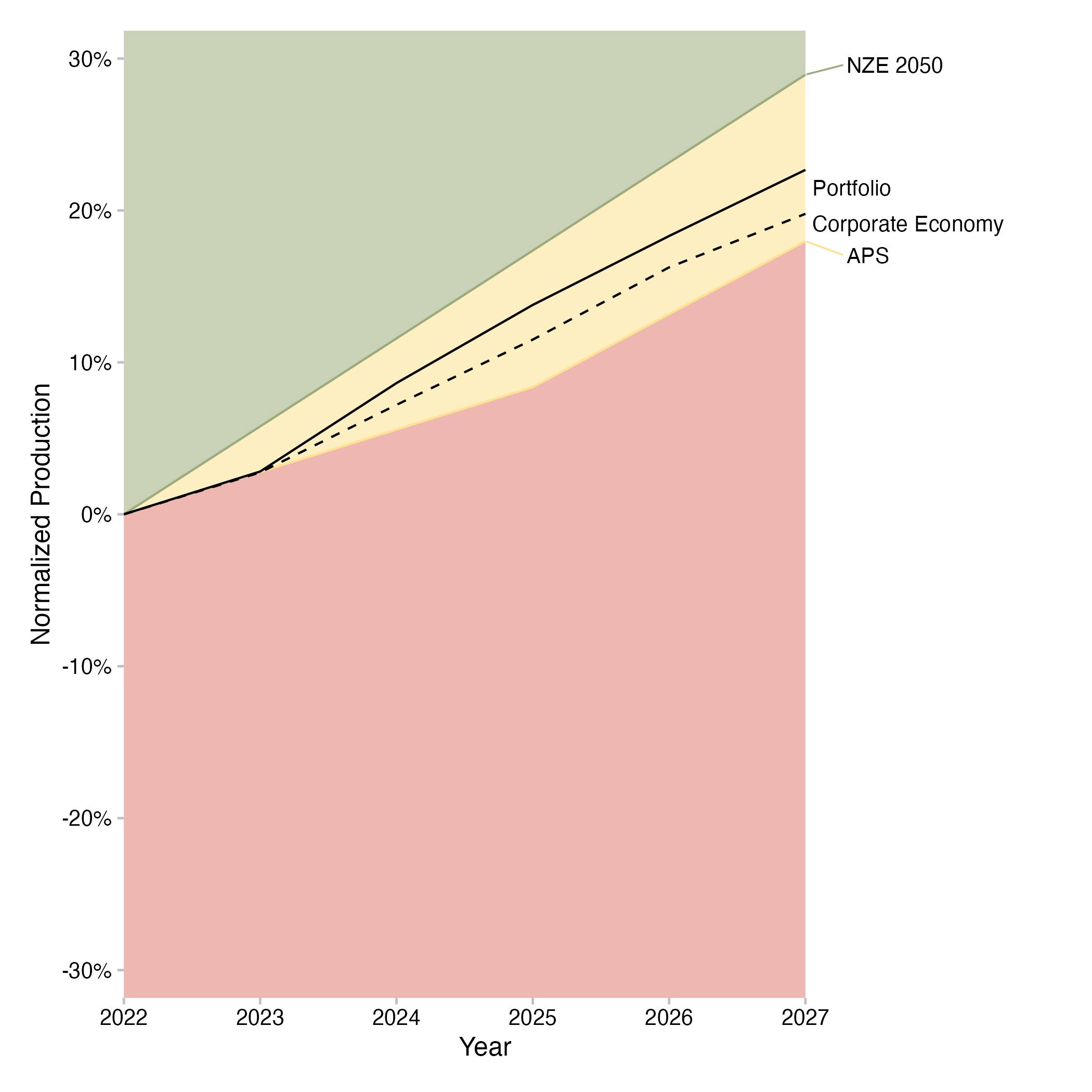

In this example of the volume trajectory plot for electric vehicle production in the automotive sector, we can see that the exposure to electric vehicle production in the loan book is projected to increase from 2022 to 2027. Electric vehicle production in the real economy is projected to increase as well, but at a slower pace. The scenario trajectories for the IEA NZE by 2050 and IEA APS for the portfolio are also shown, based on the market share approach. The projection of the portfolio falls between the APS and the NZE by 2050 trajectories.

Fig. 8: Volume trajectory plot for electric vehicle production in the automotive sector of a loan book. Data is based on simulated test loan books.

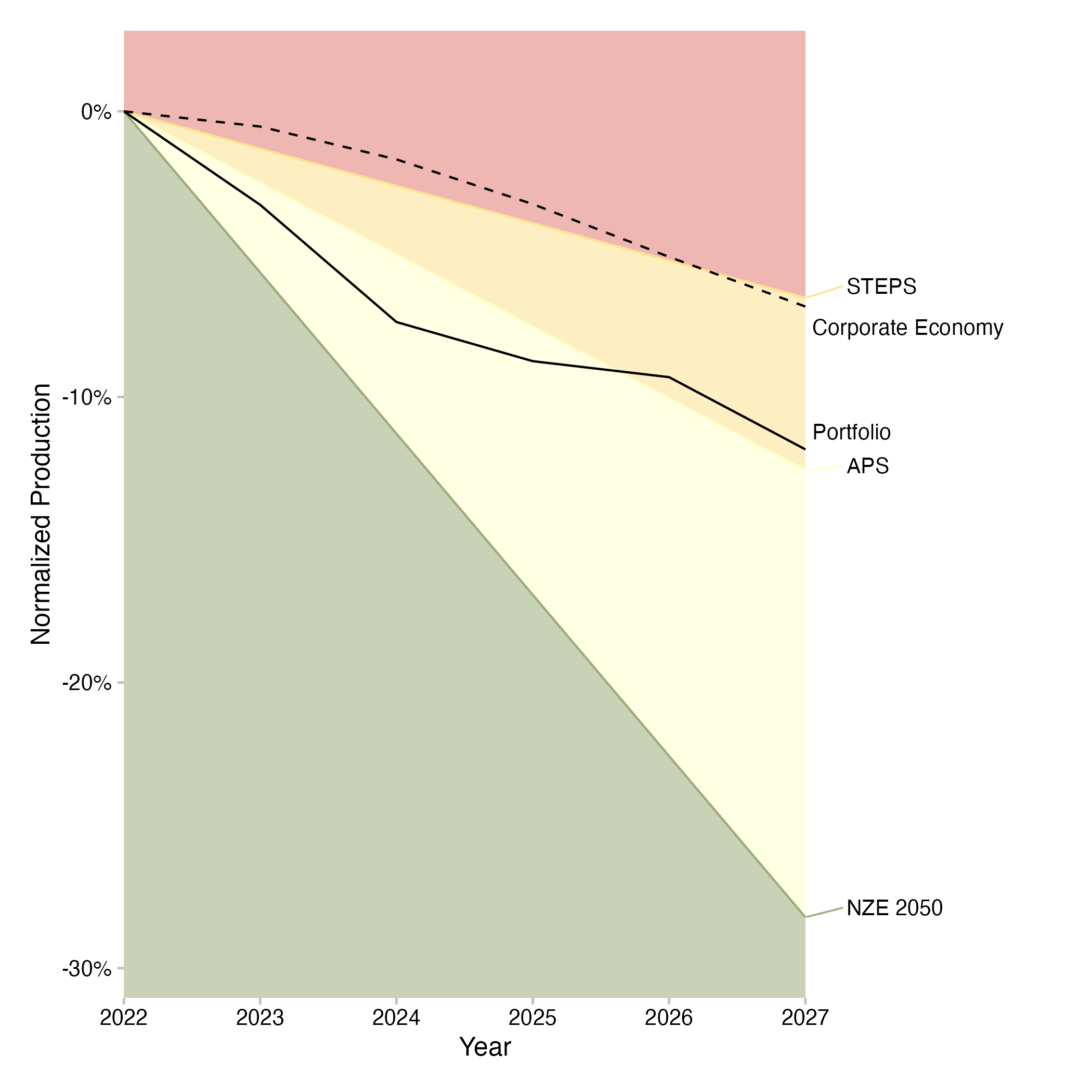

In another example of the production volume trajectory plot for the coal mining sector, we can see a loan book that reduces its exposed to coal mining activity over the time frame of the analysis. The real economy does so too, but again a t a slower pace. The scenario trajectories for the loan book based on the market share approach are plotted for the IEA STEPS, the IEA APS, and the IEA NZE by 2050 scenarios. The trend of the loan book projection follows the APS trajectory relatively closely over the examined time frame.

Fig. 9: Volume trajectory plot for for coal mining (technology and sector) of a loan book. Data is based on simulated test loan books.

Interpretation of the Production Volume Trajectory Plots

The production volume trajectory plots show the exposure of the loan book to production capacity trends of the financed companies for a given technology over the next five years, showing changes in percent relative to the start year. It contrasts this trend with the production trend of the real economy and with the trajectories that the loan book would have to finance in order to be aligned with scenarios based on the market share approach. The shading of the graph represents the direction of the required changes based on the scenario. If the green area is at the top of the graph, the technology needs to increase over time to align with the scenario. If the red area is at the top of the graph, the technology needs to decrease over time to align with the scenario. The required rates of change that apply for the individual loan book are determined using the market share approach, using the target market share ratio (TMSR) for high-carbon technologies and the sector market share percentage (SMSP) for low-carbon technologies. If the projected production trend of the loan book is equal or greater than the highest scenario line for an increasing technology, the loan book is aligned with the most ambitious scenario for that technology.

If it is below that scenario line, the loan book is misalgined with the most ambitious scenario for that technology. It may still be aligned with a less ambitious scenario. Likewise, if the projected production trend of the loan book is equal or lower than the lowest scenario line for a decreasing technology, the loan book is aligned with the most ambitious scenario for that technology. If it is above that scenario line, the loan book is misaligned with the most ambitious scenario for that technology. It may still be aligned with a less ambitious scenario.

For more information on how to calculate the TMSR and the SMSP, see the PACTA for Banks documentation.

Also notice that alignment for one technology of a sector does not imply alignment of the entire sector. For example, building out electric vehicle production capacity in line with the IEA NZE by 2050 scenario does not say anything about the alignment of internal combustion engine production capacity. If ICE production does not decrease sufficiently fast, the sector as a whole will not be aligned. This would show both in the technology mix chart, where the slow decrease in ICE production would depress the share of EV production and in the production volume trajectory for the ICE production capacity.

Data Dictionary Production Volume Trajectory

The underlying data set used to generate the production volume trajectory plots contains the following information:

Mapping the Data Dictionary to the Production Volume Trajectory Plots

The variables in the table map to the figures as follows:

-

<by_group>:The variable that the loan books are split by. This determines the group for which the production volume trajectory is shown. E.g. in case the aggregate loan book is displayed as in figures 8 and 9, the variable and value will be “meta”. If the calculation had been grouped bybank_type, the resulting plots would have been returned for groups, such as credit unions, less significant institutions and significant institutions. -

sector: The PACTA sector that the production volume trajectory is shown for. -

technology: The technology within thesectorthat the production volume trajectory is shown for. -

year: The production volume trajectory displays annual rates of change of production volume relative to the start year, with the x-axis showing the years of the analysis. -

scenario_source: The scenario source that the production volume trajectory is shown for. This is the source set in theconfig.ymlfile. The scenario source determines the scenarios that are shown in the plot. Generally all scenarios available for thesectorandtechnologyare shown and they are represented by the lines that delineate the colored areas in the plot. -

metric/label: The metric differentiates the types of lines shown in the production volume trajectory plot.projectedrefers to the production volume trajectory of the exposures in the loan book,corporate_economyrepresents the production volume trajectory of the real economy for the selected region andtarget_<scenario>refers to the production volume trajectory the loan book would need to achieve five years into the future in order to be aligned with the scenario based on the market share approach.<scenario>will take all values of scenarios that are available for thesectorandtechnologyin thescenario_ _source. Thelabelis the same as themetric, but with a more human readable name to be displayed in the plot. -

percentage_of_initial_production_by_scope/value: The actual value that determines the direction of the lines. Thepercentage_of_initial_production_by_scopeis the percentage of the initial production volume that the production volume in the future represents. Hence, a positive value implies a build out of the underlying production capacity and a negative value stands for a decrease of production capacity. Thevalueis the same as thepercentage_of_initial_production_by_scope, but formatted for display in the plot.

Sectoral Decarbonization Approach Results

The sectoral decarbonization approach (SDA) results provide the

intermediate format output required to generate the emission intensity

plot. The output data set can be found in the

../analysis/standard/sda_results<...>.csv file, where

<…> will be replaced with the name of the variable set in the

by_group parameter.

More information on the SDA results data set can be found in the data dictionary.

Emission Intensity Pathway

The emission intensity metric compares the future emission intensity

per real economic output unit in a given sector of the companies in the

loan book with that of the companies in the wider economy and the

scenario trajectories for the loan book five years into the future,

based on the SDA approach. The output data set can be found in the

../analysis/standard/<...>/data_emission_intensity_<sector>.csv

file, where <…> will be replaced with the names of each of the

groups in the variable set in the by_group parameter. This

means that the emission intensity results always only show results for

one group at a time.

The emission intensity metric can be calculated for any sector that has sector level physical emission intensity pathways, defined as absolute emissions divided by absolute real economic output. This is usually available for a broader range of sectors than technology level pathways, including for the so called hard-to-abate sectors, where low carbon alternatives to the most commonly used production technologies are often not available yet, or at least not market ready.

As the emission intensity metric is compared to scenario values based on the SDA approach, the calculation of the scenario values for each portfolio follows different rules than the market share approach used in the technology mix and the production volume trajectory. The SDA approach is a convergence approach and does not necessarily require stable market share for all companies and/or loan books. Rather, it requires that all participants in a sector approach the same emission intensity target at the end year of the scenario. Notice that the end year of the scenario is usually much farther in the future than the five year forward looking horizon of the analysis, which is why the loan book value is not expected to have converged with the scenario value after five years.

LINK to some more general SDA/EI explanation?

Example Plots Emission Intensity Pathway

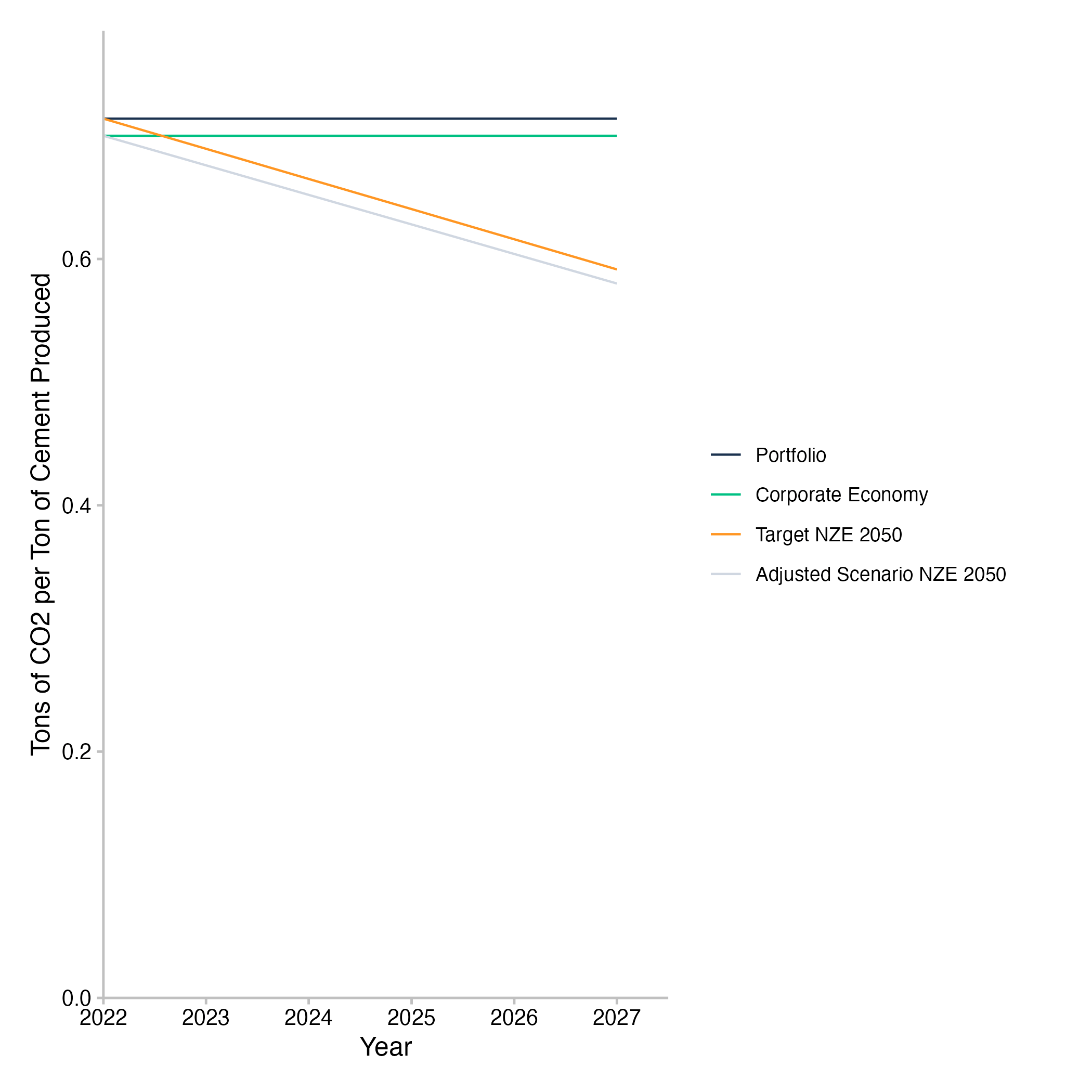

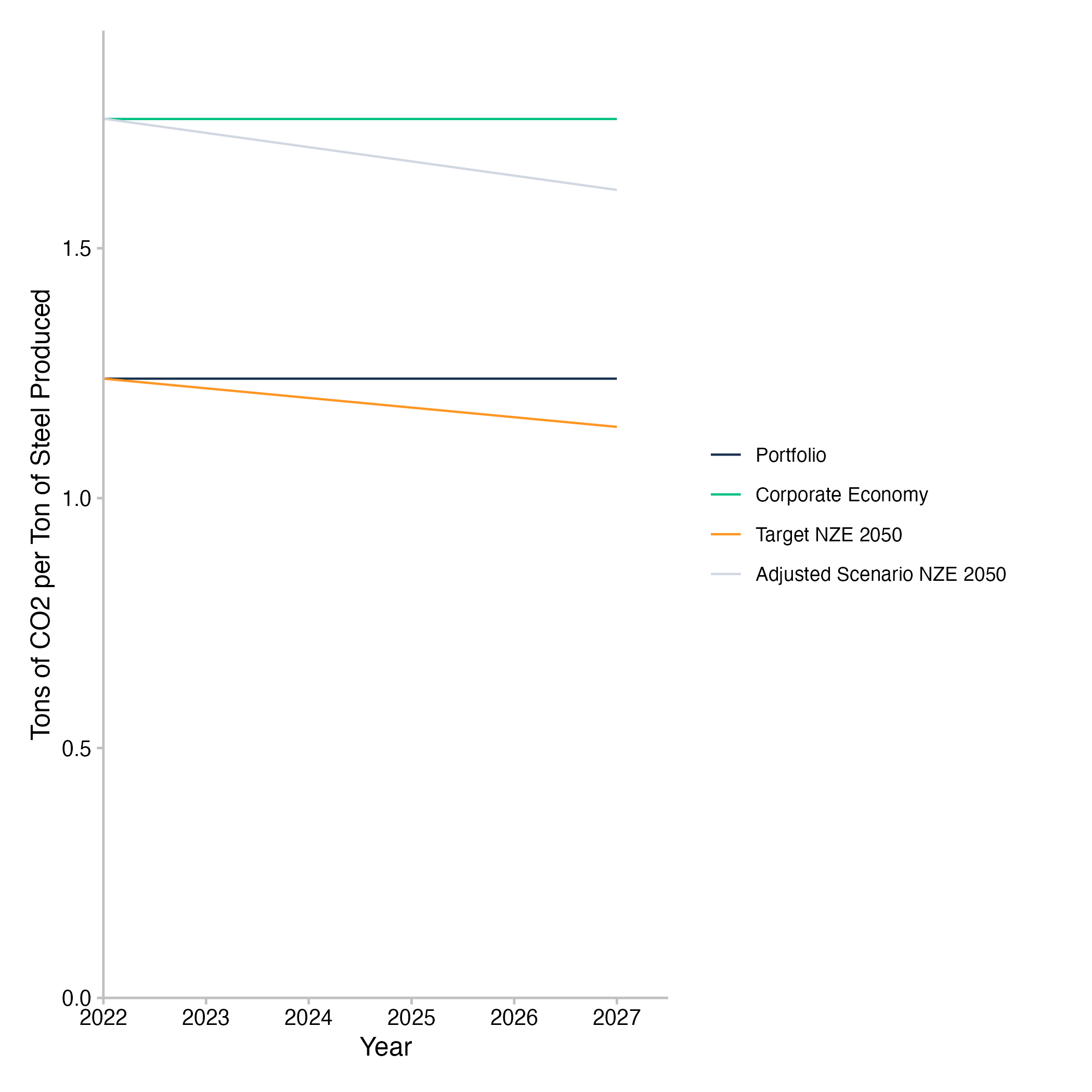

This example of the emission intensity pathway plot for cement production shows that the emission intensity of the companies the loan book is exposed to remain relatively stable at a higher level than that of the wider economy over the next five years. It also shows that both the target for the loan book based on the IEA NZE by 2050 scenario and the adjusted target for the wider economy based on the same scenario decrease over that time frame. The specific pathways of both these scenario trajectories converge in the end year of the scenario calculation - in this case 2050 - because they were calculated using a convergence approach, the SDA approach.

Fig. 10: Emission intensity pathway plot for cement production of companies in the loan book. Data is based on simulated test loan books.

In another example of the emission intensity pathway plot for the steel sector, we can see a loan book with an emission intensity based on its steel company exposure that is below the emission intensity of the real economy. Again, the trend of the emission intensity for both the companies in the loan book as well as the wider economy is rather stable and both would need to decrease over the next five years in order to be aligned with their respective scenario pathways, based on the SDA approach. This also again implies that the target scenario pathway of the loan book and the corporate economy converge in the end year of the scenario calculation.

Fig. 11: Emission intensity pathway plot for steel production of companies in the loan book. Data is based on simulated test loan books.

Interpretation of the Emission Intensity Pathway Plots

The emission intensity pathway plots show the physical emission intensity trajectory of the portfolio weighted companies that the loan book is exposed to and contrast this with the physical emission intensity pathway of all companies in the relevant region of the real economy. Physical emission intensity in this case refers to the amount of CO2(eq) emissions per unit of real economic output from the sector at hand. Since the units of output are interchangeable per sector, but not across sectors, the physical emission intensity is a useful sector level metric. Since the emission intensity metric does not require technology level production pathways to be available, it can be used for sectors that do now have market-ready low carbon alternatives to replace high-carbon technologies yet. For the PACTA sectors, this is the case for the hard-to-abate sectors, such as cement, steel, and aviation. It can be applied to all other PACTA sectors as well though, although it may not be equally meaningful in all cases (for example, for a phaseout of coal mining, the emission intensity of coal mining may not be the most actionable metric).

The emission intensity of different loan books will vary within the same sector, depending on the companies that the loan books are exposed to. Accordingly, the effort required by each of the banks to align their loan books with the target scenario in that sector will differ as well. With the SDA approach being a convergence approach, any loan book with a higher than average emission intensity will be expected to follow a steeper decline in emission intensity than a loan book with a lower than average emission intensity. This is a necessary requirement of the convergence approach to scenario allocation. However, the initial level of the physical emission intensity of the loan book does not impact the alignment of the loan book. Whether or not alignment is achieved, depends solely on the rate of change of the emission intensity relative to the loan book specific decarbonization pathway.

Data Dictionary Emission Intensity Pathway

The underlying data set used to generate the emission intensity pathway plots contains the following information:

Mapping the Data Dictionary to the Emission Intensity Pathway Plots

The variables in the table map to the figures as follows:

-

<by_group>:The variable that the loan books are split by. This determines the group for which the emission intensity pathway is shown. E.g. in case the aggregate loan book is displayed as in figures 10 and 11, the variable and value will be “meta”. If the calculation had been grouped bybank_type, the resulting plots would have been returned for groups, such as credit unions, less significant institutions and significant institutions. -

sector: The PACTA sector that the emission intensity pathway is shown for. -

year: The emission intensity pathway displays annual physical emission intensities, with the x-axis showing the years of the analysis. -

scenario_source: The scenario source that the emission intensity pathway is shown for. This is the source set in theconfig.ymlfile. -

emission_factor_metric/label: The metric differentiates the types of lines shown in the emission intensity pathway plot.projectedrefers to the emission intensity of the loan book based on its exposures to the underlying companies,corporate_economyrepresents the emission intensity of the companies in the real economy,target_<scenario>refers to the emission intensity pathway the loan book would need to follow to remain aligned with the scenario based on the SDA approach, andadjusted_scenario_<scenario>is the emission intensity pathway the corporate economy in the sector would need to follow to remain aligned.<scenario>stands for the selected target scenario as set in theconfig.ymlfile. Thelabelis the same as theemission_factor_metric, but with a more human readable name to be displayed in the plot. -

emission_factor_value: The actual value that determines the points that the emission intensity lines follow in the plot. Theemission_factor_valueis the ratio of emissions per real economic output unit.

Net Aggregate Alignment Metric Outputs and Graphs

This section provides a description of the data outputs and graphs related to the Net Aggregate Alignment Metrics. Some of the data outputs are intermediate files that do not directly map to a plot. Such outputs are explained in detail in the data dictionary. The plots are discussed in more detail, including the relevant table from the data dictionary and how the variables map to the plots.

Please note that all plots in this section build on the Net Aggregate Alignment Metric, which is an aggregation of PACTA results for every sector that allows for a high level overview of sector alignment at the loan book level or higher. An intended use case is to use this metric first at the aggregate financial system level across all loan books and then drill down along different dimensions of interest. The idea behind this approach is to facilitate the comparison of many different banks and loan books using forward-looking production based alignment metrics without producing an excessive amount of plots and results that becomes hard to navigate and that may not reveal higher level patterns easily. The Net Aggregate Alignment Metric was first developed in the ECB Banking Supervision paper “Risks from misalignment of banks’ financing with the EU climate objectives - Assessment of the alignment of the European banking sector”. For a detailed description of the methodology used in this implementation of the Net Aggregate Alignment Metric, see the two-part documentation here (company level) and here (loan book level).

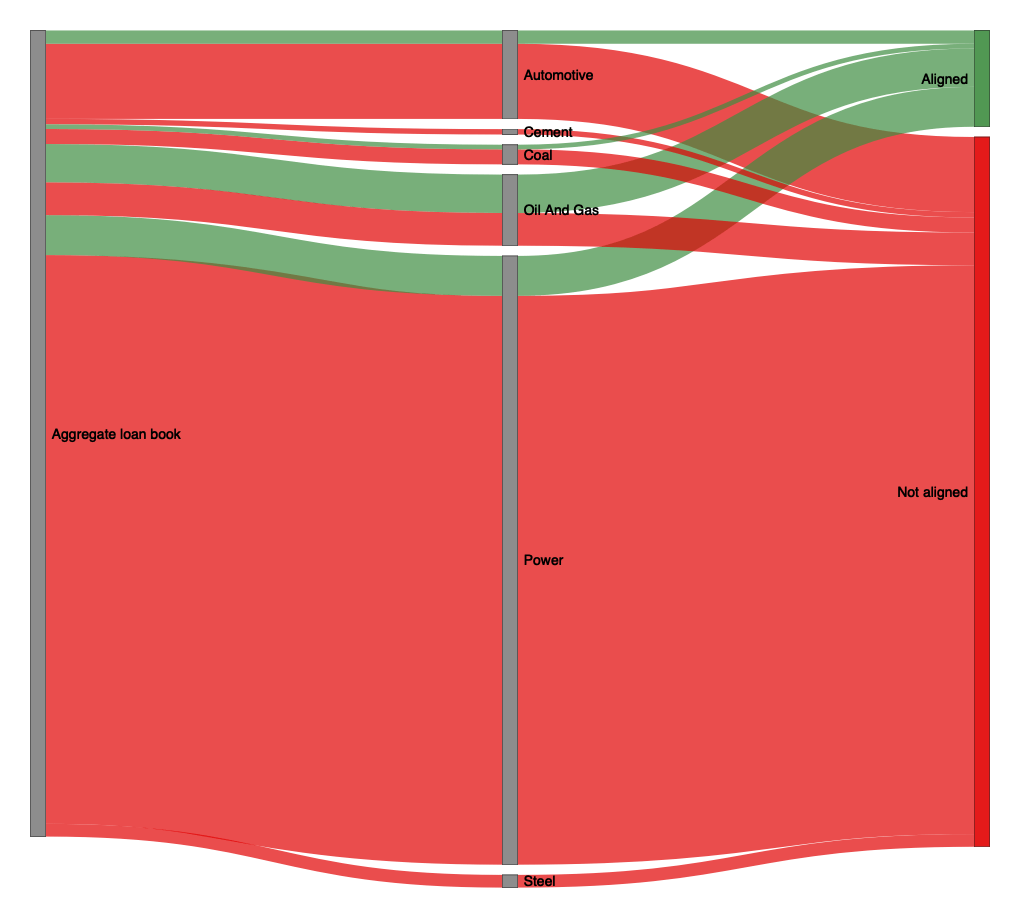

Net Aggregate Alignment Metric - Sankey Plot

The net aggregate alignment sankey plot summarizes the financial

exposure of a (grouped or ungrouped) loan book (left node) by financial

exposure to PACTA sectors (middle node) and finally by whether or not

the exposures are aligned based on the net aggregate alignment metric

(right node). Alignment is defined as a binary variable, where any

underlying exposure with an alignment metric greater or equal to 0 is

considered aligned and any exposure with an alignment metric less than 0

is considered misaligned. The main purpose of this type of visualization

is to provide an overview of system level alignment at one quick glance,

at the expense of some detail that can be obtained from other plots. The

output data set can be found in the

../analysis/aggregated/data_sankey_sector<...>.csv

file, where <…> will be replaced with the names of each of the

groups in the variable set in the by_group parameter.

Example Plots Net Aggregate Alignment Metric - Sankey Plot

This example of the sankey plot looks at the aggregate financial exposure of all analyzed loan books (figure 12, left node). The middle node shows that a large share of the financial exposure can be found the in the power sector, with the automotive and oil & gas sectors also contributing significant chunks. Cement, coal and steel contribute minor parts to the overall financial exposure. The right node, in turn, shows how the sector exposure is distributed with regard to a binary alignment metric, based on the net aggregate alignment metric. Overall, green ribbons indicate the size of the aligned exposure, while red ribbons indicate the size of the misaligned exposure. We can see that aligned exposures make up a much smaller share of the overall exposure than misaligned exposures. The distribution of alignment/misalignment furthermore varies significantly between sectors, with half the exposure value in the oil & gas sector aligned, a much higher share than in any other of the sectors. The nature of this plot as a high level overview means that it does not show all the details. For example, the underlying companies are classified as aligned or misaligned in a binary manner. The net aggregate alignment metric is a continuous variable though, so the binary representation may skew the extent of alignment to some degree and should always be complemented with additional analyses from the following plots.

Fig. 12: Sankey plot of the aggregated loan books by sector and by net aggregate alignment metric. Data is based on simulated test loan books.

Interpretation of the Sankey Plot

The sankey plot emphasizes the distribution of the financial exposure of the analyzed loan books across sectors and aligned or misaligned counterparties. The plot necessitate categorical variables for the types of nodes, which means that the net aggregate alignment metric is transformed into a binary variable. The size of each group in a node along the y axis is the financial exposure to that group and that is the only continuous variable in this plot. In effect, the statements you can make based on this plot are along the lines of “XY USD of the financial exposure of the loan books is concentrated in the power sector. Among the exposure to power companies, the largest share goes to companies that are misaligned with the selected scenario”. As we can see, this reveals more about howw much money is lent to how many companies that are misaligned ins oem form. It says nothing about how misaligned these companies are. They might all be very close to, but just behind, the scenario target. Or they might all be grossly off target. The reason why this is still a useful plot is because you get a very quick over view, in which sectors are the largest shares of your misaligned companies. This makes it easier to prioritize which company analytics to look at first. Additionally, you can validate the severity of the misalignment in a given sector, by inspecting the alignment-by-exposure plots, which will be explained next.

Data Dictionary Net Aggregate Alignment Metric - Sankey Plot

The underlying data set used to generate the net aggregate alignment sankey plot contains the following information:

Mapping the Data Dictionary to the Sankey Plot

The variables in the table map to the figures as follows:

-

<by_group>: The variable that the loan books are split by. This corresponds to the leftmost node in the sankey plot and the values can either be all the same for the aggregate view on all analysed loan books or the values corresponding to each of the groups. -

middle_node: The PACTA sectors for which there is some financial exposure in the analyzed loan books. -

is_aligned: Binary variable that can have values “aligned” or “not aligned”. All exposures that are aligned are represented as green ribbons, all those that are not aligned are red ribbons. The underlying net alignment metric refers to the five year forward-looking values in the final year of the analysis. -

loan_size_outstanding: The financial exposure of the loan books to the individual sectors and grouped byìs_aligned. This is the continuous variable that determines the size of the ribbons in the plot along the y-axis.

Net Aggregate Alignment by Financial Exposure

The net aggregate alignment by financial exposure plot summarizes the

financial exposure (y-axis) of a (grouped or ungrouped) loan book (dot

color) by financial exposure to PACTA sectors (x-axis). Every sector is

shown in a separate pane with equal scales, which allows comparing the

significance of exposures across sectors. In this plot, the net

aggregate alignment metric is presented as a continuous variable along

the y axis, which allows for more nuance compared with the sankey plot.

Exposures to very misaligned companies will influence the loan book

level alignment more negaatively here, because the loan book level net

aggregate alignment metric is a weighted mean of the underlying

continuous company level net aggregate alignments weighted by the

financial exposure. However, this addittional detail makes the plot

slightly slower to read than the sankey plot. Generally, this plot

emphasizes the scale of the net aggregate alignment more than the

exposure and is therefore a good complementary plot to the sankey plot.

The output data set can be found in the

../analysis/aggregated/data_scatter_alignment_exposure<...>.csv

file, where <…> will be replaced with the names of each of the

groups in the variable set in the by_group parameter.

Example Plots Alignment by Exposure

In this example plot, we analyse the net aggregate alignment by different bank types across six of the PACTA sectors. It is immediately obvious, that the exposures of credit unions in the oil & gas sector (misaligned) and in the power sector (aligned), as well as the exposures of less significant institutions in the coal sector (misaligned) have very pronounced net aggregate alignment metrics. This can be a further avenue for research into which specific companies seem to drive these results. It is also evident, that this plot does not make it very easy to compare the financial exposures across sectors, which highlights again one of the strengths of the sankey plot. Within sector however, financial exposure between groups can easily be differentiated.

Fig. 13: Alignment by exposure plot of loan books grouped by bank type. Data is based on simulated test loan books.

Interpretation of the Alignment by Exposure Plots

Generally, the alignment by exposure sector is very useful for interpretations of net alignment within sectors. Groups (e.g. bank types, but possibly other types of groups) further to the right of the x-axis have a larger financial exposure to companies in this sector than other groups. Dots higher on the y-axis indicate groups for which the loan book level net aggregate alignment is further ahead of the scenario than for groups with a dot lower on the y-axis. The 0 intercept on the y-axis means the weighted average net aggregate alignment of the group is right on target.

Of course, since the net aggregate alignment at loan book level is a

weighted average of the underlying company level net aggregate

alignments, a positive y-value does not mean that there are no

misaligned companies to be found in the loan book for this sector. If

individual company level alignment is of concern for your use case, you

will have to check company level results to validate that. The most

comprehensive output data set to inspect company level net alignment

metrics is the

../analysis/aggregated/company_exposure_net_aggregate_alignment<...>.csv

file. Documentation for its contents can be found here.

Data Dictionary Alignment by Exposure

The underlying data set used to generate the net aggregate alignment by financial exposure plot contains the following information:

Mapping the Data Dictionary to the Alignment by Exposure Plots